back back

last

ecostory

last

ecostory  2/2011

next

2/2011

next E

home

E

home

|

World Oil Capacity to Peak in 2010 Says Petrobras CEO

|

ecoglobe received this story in the second week of 2011, when we were gearing up to spread the inconvenient and scaring energy messages.

In 2009 the newspapers reported on the opinions held by the CEO of Petrobras (Brazil), as well as the PDG of Total (France), both stating that oil production is peaking. In 2009 the newspapers reported on the opinions held by the CEO of Petrobras (Brazil), as well as the PDG of Total (France), both stating that oil production is peaking.

Business and politics, however, took no notice. Neither did they after the publication of the last Energy Outlook by the IEA, which for the first time in their existence uses the expression Peak Oil.

Below story and graphs are clear. If in doubt, ask or simple give us your feedback!

|

Thanks to George Taylor for this article about a talk given by the CEO of Petrobras (Brazilian oil company) in December 2009. Posted on February 4, 2010 on: www.theoildrum.com/node/6169.

World Oil Capacity to Peak in 2010 Says Petrobras CEO

Jose Sergio Gabrielli, CEO of Petrobras, gave a presentation in December 2009 in which he shows world oil capacity, including biofuels, peaking in 2010 due to oil capacity additions from new projects being unable to offset world oil decline rates.

Gabrielli states that the world needs oil volumes the equivalent of one Saudi Arabia every two years to offset future world oil decline rates.

This is a stronger statement than the one he gave in January 2009 in an interview with Business Week when he said the following.

According to the company's projections, production from existing fields will fall from a little over 80 million barrels a day to maybe half of that even if new techniques are used to slow their rate of decline. So just keeping global production flat is going to require lots of new fields and requires the world to replace one Saudi Arabia per three years.

Gabrielli is clearly concerned about declining future world oil production. His statements are now in alignment with those of other oil company executives including Sadad al-Husseini, former Aramco executive, who states that world oil production is on a peak plateau, and Total's CEO, Christophe de Margerie who doesn't see global oil production ever exceeding 89 million barrels per day (mbd). World oil production in December 2009 was only slightly lower at 86 mbd.

Gabrielli shows world oil capacity peaking in 2010 as shown in the translated version of his chart below. He shows historical world oil production to 2008. Next, he applies a decline rate of 5% per year to existing production represented by the lower light blue area. He then forecasts capacity additions from sanctioned projects estimated from Wood MacKenzie's Global Oil Supply Tool. These oil capacity additions are in four categories: OPEC new projects, OPEC expansion projects, non-OPEC new projects and non-OPEC expansion projects. In 2010 the biggest contributor is OPEC expansion projects which includes about 1.3 mbd from Khurais and 0.8 mbd from Khursaniyah. These additions include both crude oil and natural gas liquids and are sourced from Saudi Arabia's official statements which lack independent verification.

He also shows three demand scenarios ranging from low demand to high demand. For the BAU scenario, the required new capacity, in addition to sanctioned project capacities, is about 29 mbd in 2020. Unsanctioned projects from Brazil and Iraq should be able to provide some of this capacity but other capacity additions will be needed to meet demand. Biofuels can also help but there will probably not be enough new oil capacity additions to meet demand in 2020.

It is important to note that Gabrielli's capacity additions exclude additions from unsanctioned projects and from oil yet to be discovered. Thus many Iraq projects and Brazilian Santos basin projects would be excluded. Iraq might produce another 8 mbd by 2020 according to recent estimates by BP's CEO. Brazil's production is forecast by Petrobras to increase by about 2 mbd by 2020. Thus, additions from non sanctioned projects from Iraq and Brazil might add another 10 mbd capacity by 2020. However, this still leaves a required lower capacity addition of 19 to 24 mbd in 2020 to come from other sources. This capacity addition is equivalent to production from about two Saudi Arabias which is an enormous challenge.

Gabrielli's observed decline rate appears to be about 5% per year and he applies it to the entire liquids production in 2008. Part of the liquids production, such as ethanol and Canada oil sands, is increasing rather than declining. The use of separate decline rates for each component of liquids production would be better, but the peak oil capacity year of 2010 would probably not change. Instead, the forecast production curve decline profile would be slightly different.

Fig 1 - World Oil Capacity and Demand to 2030 (oil includes crude oil, lease condensate, oil sands, natural gas liquids, biofuels and refinery processing gains)

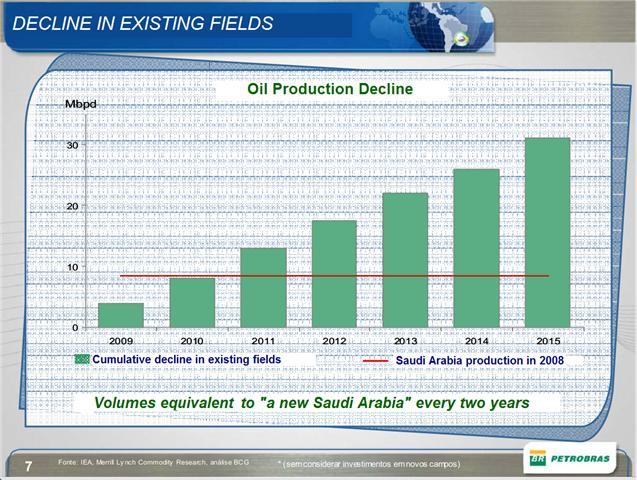

On another slide, Gabrielli plots cumulative decline in existing fields against time. Consequently, the world needs one Saudi Arabia every two years just to keep production constant. Fortunately, new oil capacity from sanctioned projects can offset some of cumulative decline of 30 mbd in 2015. However, the chart above still shows a gap of over 5 mbd which needs to be filled by projects yet to be sanctioned or development of undiscovered oil. If this gap cannot be filled then demand cannot be met and prices will increase to reduce demand down to supply.

Fig 2 - One Saudi Arabia Needed Every Two Years

Gabrielli also shows few new large discoveries being made recently in the chart below. However, these discoveries can have significant lag periods before production reaches meaningful levels. Petrobras' recent discovery at Tupi may be about 5 billion barrels of oil and gas, but production is expected to grow slowly with capacity increasing to 100,000 barrels per day possibly by the end of this year. This capacity is planned to remain constant until 2012 as part of the Tupi pilot project. If full commerciality is declared, then Tupi might reach 1 mbd by 2022. Gabrielli also shows the large Kashagan discovery in 2000 which was supposed to start production in 2005, but the earliest start date is now 2013.

Additional constraints on world oil production are weaknesses in the production, refining and logistics systems. In addition, Gabrielli points out that refineries need to be matched to the type of oil being produced. Recently, world oil production is becoming heavier and more sour which requires suitable refineries. The construction of these refineries can take several years. Limitations of known reservoirs are an additional constraint as many existing fields are very old and cannot produce more oil easily. Mexico's Cantarell field is in decline and Kuwait's Burgan field has passed peak production.

Fig 3 - Recent Large World Oil Discoveries

In October 2009, Gabrielli gave a different presentation which showed a forecast of world oil demand based on the IEA WEO 2008 and the EIA IEO 2009 shown below. Note that the additional capacities required for 2020 and 2030 are larger than the ranges given in his December 2009 presentation. For example, in 2020, Fig 1 shows additional required capacity of 29 to 34 mbd while Fig 4 shows required capacity of 42 to 51 mbd. This difference is due to Fig 4 excluding sanctioned project additions, whereas Fig 1 includes sanctioned project additions as sourced from Wood MacKenzie. Gabrielli expresses concern about future oil supply as he states in the slide below that world oil production capacity will be challenged to meet projected demand growth.

Fig 4 - World Oil Demand to 2030 (oil includes crude oil, lease condensate, oil sands and natural gas liquids)

|

|

Gabrielli's concerns about peak oil capacity in 2010 and future declining world oil capacity should be taken seriously. In Fig 1 above, he shows that by 2012/13 the world oil capacity will only just meet world demand, based on Wood MacKenzie's data, highlighting the risk of a potential oil supply crunch. If Wikipedia Oil Megaproject data are used then peak oil capacity is also indicated in 2010 as well as an oil supply crunch in 2012/13. The IEA's Fatih Birol has also stated that an oil supply crunch is likely to occur by 2014. In other words, the world does not have enough future Saudi Arabia equivalent capacity additions to stop world oil production from declining, causing an inevitable supply crunch within the next few years.

Gabrielli's concerns about peak oil capacity in 2010 and future declining world oil capacity should be taken seriously. In Fig 1 above, he shows that by 2012/13 the world oil capacity will only just meet world demand, based on Wood MacKenzie's data, highlighting the risk of a potential oil supply crunch. If Wikipedia Oil Megaproject data are used then peak oil capacity is also indicated in 2010 as well as an oil supply crunch in 2012/13. The IEA's Fatih Birol has also stated that an oil supply crunch is likely to occur by 2014. In other words, the world does not have enough future Saudi Arabia equivalent capacity additions to stop world oil production from declining, causing an inevitable supply crunch within the next few years.

populationmedia.org

PMC website: www.populationmedia.org

PI website: www.populationinstitute.org

populationmedia.org

PMC website: www.populationmedia.org

PI website: www.populationinstitute.org