back back

previous

ecostory

previous

ecostory

54/2011

next

54/2011

next E

home

E

home

IEA World Energy Outlook 2011

and its growth scenario till 2035

|

[IEA 2010 World Energy Outlook

IEA 2012 World Energy Outlook]

Highlight at the UNECE Energy Week was

IEA's Chief Economist, Dr. Fatih Birol, with his presentation of the IEA World Energy Outlook.

The presentation largely followed the line of last week's press conference and press release

ecoglobe raised its usual sustainability point in two questions to Fatih Birol.

[reminder:]

"Sustainability" means human society

in the balance with nature.

The balances are maintained if a resource is not consumed at a higher rate than needed for regeneration.

Many resources are non-renewable.

So here we must judge very carefully at which speed we may reasonably use these.

All resources - regenerative and non-renewable - are horribly over-exploited. (Overshoot)

Sustainability excludes growth, as explained below.

The IEA's 2011 peak oil assessment seems being hugely different form last year's

|

Letter to Dr Fatih Birol:  [ [ ] ]

ecology discovery foundation - ecoglobe

Helmut E. Lubbers

BE MsocSc DipEcol

14 Boulevard Carl-Vogt

CH-1205 Genève / Genf

Schweiz/Suisse/Svizzera

|

helmut ecoglobe.ch ecoglobe.ch

www.ecoglobe.org

www.ecoglobe.ch

|

Genève/Genf, 16 November 2011

Lu/rs/ieab1n16

|

ecoglobe, 14 bd. Carl-Vogt, CH-1205 Genève

Dr Fatih Birol

Chief Economist International Energy Agency

9 rue de la Fédération

75739 Paris Cedex 15

France

|

The world energy outlook and its growth scenarios

Dear Dr. Birol,

after your most interesting presentation of this morning, for wich I thank you very much, I asked the questions (1) why the IEA scenarios always assume further growth and (2) why they stop at 2035, as if the world would then finish.

I suggested that the earth can not support (more) growth for environmental reasons, i.e. depletion and destruction of non-renewable resources and nature, leading to increasing scarcities. []

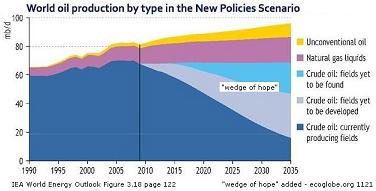

I forgot my question about Peak Oil, which the IEA mentioned last year, with this graph in which the yet to be discovered and yet to be developed crude oil fields were apostrophed as "the wedge of hope" (ASPO). Does the IEA not consider the distinct possibility of an industrial and food production downslope after Peak Oil? You may compare ecostory 7/2011 on the Future of the WTO after Peak-Oil.

I forgot my question about Peak Oil, which the IEA mentioned last year, with this graph in which the yet to be discovered and yet to be developed crude oil fields were apostrophed as "the wedge of hope" (ASPO). Does the IEA not consider the distinct possibility of an industrial and food production downslope after Peak Oil? You may compare ecostory 7/2011 on the Future of the WTO after Peak-Oil.

The 2011 World Energy Outlook states "Crude

oil production – the largest single component of oil production – increases marginally to a

plateau of around 69 mb/d (slightly below the historic high of 70 mb/d in 2008) and then

declines slowly to around 68 mb/d by 2035." (page 122, Chapter on "Global Energy Trends).

Extending your last year's production plateau to 2035 signals your belief that those oil fields in the wedge of hope will eventuate. How certain is this?

A related question is whether the IEA considers the effect of decreasing EROEI - Energetic Return On Energetic Investment. Increasing technology requirements lead to a decreasing EROEI. When we need more energy for oil extraction than the net energy available in the end product, crude oil extraction becomes a loss-making activity. Some specialists say that the break-eaven point lies at an EROEI of 5:1, because this energy EROEI is needed for maintenance. The present EROEI is estimated to lie around 25:1, a quarter of 100 years ago.

To my questions raised after your presentation you replied the following: []

1. Growth is needed for poor countries. Africa is an example. We cannot tell them to stop, if we compare their lifestyle with the Swiss.

2. We can grow more efficiently [i.e. growing whilst using less resources.]

Both your answers are common reactions to voices that point at the finiteness of the planet.

Regrettably they are both incorrect, because:

1. Poverty alleviation and better lifestyles do factually increase the pressure on the lands locally. The local population suffers from the negative effects. Economic development (growth) and population growth always lead to higher environmental problems and scarcities, never mind whether that occurs in Switzerland or in Kenya or Nigeria or anywhere.

Any amelioration of living conditions of the very poor must be offset by more frugal lifestyles of the wealthier part of a population or country. Anything else is not sustainable, cannot continue for a long time.

2. Increasing efficiences do not influence the effect of growth. GDP and population growths are always material. If we use less material for the same product or service, then the GDP will decrease. Other statements flout the realities of GDP accounting.

Your answers did not address the question of long-term scenarios, after 2035, i.e. the assumption most people unwittingly make that all other conditions will remain the same ("ceteris paribus" - all other things equal).

Surely conditions are changing, such as the effects of unstoppable climate change, deforestation, overfishing, decreasing biodiversity, overgrazing, soil fertility, potable water availability, and the industrial and agricultural output decreases on the PPOD, the Post Peak Oil Downslope.

The question "after 2035" must be asked:

What will we do when we have found and exploited all fossil energy sources?

Can technology really revive extinct species, repair environmental damage or replenish depeleted mineral resources?

Environmental scientists do not believe that we have the skills of Mr Houdini, who could reportedly shake off all shackles, as one speaker suggested in a presentation - after displaying the below Global Energy Trends (source: IEA).

Environmental scientists do not believe that we have the skills of Mr Houdini, who could reportedly shake off all shackles, as one speaker suggested in a presentation - after displaying the below Global Energy Trends (source: IEA).

Our globe does not grow. This Earth is inescapably chained.

Our globe does not grow. This Earth is inescapably chained.

Our realities are a finite planet with increasing speeds of resource depletion and no magician who can work miracles tomorrow.

The unsustainable trends result from economic expansion and population growth, and from technology, which speeds up exploitation rates.

Finally it needs to be pointed out that

so-called "renewable fuels" are no way out.

Firstly renewables are electricity "only" and cannot replace fossil fuels.

Secondly, even if we could replace oil, we would still continue our depletion of other resources.

Many people say "growth" but actually mean to say "jobs" and "work". Growth means more people, more stuff. In many discussions this needs to be clarified. This will enhance mutual understanding.

Given the above, which I believe being a correct, concise picture of humanity's sustainability problem, may I suggest that the IEA pays more attention to environmental conditions and longer term trends? It would certainly enhance the usability of your report by politics.

It has been privilege to meet and also having had a short private discussion.

cc: website

|

With kind regards,

[signature H E Lubbers]

|

|

|

Contact: IEA Press Office

ieapressoffice@iea.org

The world is locking itself into an unsustainable energy future which would have far-reaching

consequences, IEA warns in its latest World Energy Outlook

LONDON, 9 November - Without a bold change of policy direction, the world will lock itself into an

insecure, inefficient and high-carbon energy system, the International Energy Agency warned as it

launched the 2011 edition of the World Energy Outlook (WEO ).The agency's flagship publication,

released today in London, said there is still time to act, but the window of opportunity is closing.

“Growth, prosperity and rising population will inevitably push up energy needs over the coming decades.

But we cannot continue to rely on insecure and environmentally unsustainable uses of energy,” said IEA

Executive Director Maria van der Hoeven. “Governments need to introduce stronger measures to

drive investment in efficient and low-carbon technologies. The Fukushima nuclear accident, the turmoil

in parts of the Middle East and North Africa and a sharp rebound in energy demand in 2010 which

pushed CO2 emissions to a record high, highlight the urgency and the scale of the challenge.”

In the WEO's central New Policies Scenario, which assumes that recent government commitments are

implemented in a cautious manner, primary energy demand increases by one-third between 2010 and

2035, with 90% of the growth in non-OECD economies. China consolidates its position as the world’s

largest energy consumer: it consumes nearly 70% more energy than the United States by 2035, even

though, by then, per capita demand in China is still less than half the level in the United States. The share

of fossil fuels in global primary energy consumption falls from around 81% today to 75% in 2035.

Renewables increase from 13% of the mix today to 18% in 2035; the growth in renewables is

underpinned by subsidies that rise from $64 billion in 2010 to $250 billion in 2035, support that in some

cases cannot be taken for granted in this age of fiscal austerity. By contrast, subsidies for fossil fuels

amounted to $409 billion in 2010.

Short-term pressures on oil markets are easing with the economic slowdown and the expected return of

Libyan supply. But the average oil price remains high, approaching $120/barrel (in year-2010

dollars) in 2035. Reliance grows on a small number of producers: the increase in output from Middle

East and North Africa (MENA) is over 90% of the required growth in world oil output to 2035. If,

between 2011 and 2015, investment in the MENA region runs one-third lower than the $100 billion per

year required, consumers could face a near-term rise in the oil price to $150/barrel.

Oil demand rises from 87 million barrels per day (mb/d) in 2010 to 99 mb/d in 2035, with all the

net growth coming from the transport sector in emerging economies. The passenger vehicle fleet

doubles to almost 1.7 billion in 2035. Alternative technologies, such as hybrid and electric vehicles that

use oil more efficiently or not at all, continue to advance but they take time to penetrate markets.

The use of coal – which met almost half of the increase in global energy demand over the last

decade – rises 65% by 2035. Prospects for coal are especially sensitive to energy policies – notably in

China, which today accounts for almost half of global demand. More efficient power plants and carbon

capture and storage (CCS) technology could boost prospects for coal, but the latter still faces significant

regulatory, policy and technical barriers that make its deployment uncertain.

Fukushima Daiichi has raised questions about the future role of nuclear power. In the New Policies

Scenario, nuclear output rises by over 70% by 2035, only slightly less than projected last year, as most countries with nuclear programmes have reaffirmed their commitment to them. But given the increased

uncertainty, that could change. A special Low Nuclear Case examines what would happen if the

anticipated contribution of nuclear to future energy supply were to be halved. While providing a boost to

renewables, such a slowdown would increase import bills, heighten energy security concerns and

make it harder and more expensive to combat climate change.

The future for natural gas is more certain: its share in the energy mix rises and gas use almost catches up

with coal consumption, underscoring key findings from a recent WEO Special Report which examined

whether the world is entering a “Golden Age of Gas ”. One country set to benefit from increased

demand for gas is Russia, which is the subject of a special in-depth study in WEO-2011. Key

challenges for Russia are to finance a new generation of higher-cost oil and gas fields and to improve its

energy efficiency. While Russia remains an important supplier to its traditional markets in Europe, a shift

in its fossil fuel exports towards China and the Asia-Pacific gathers momentum. If Russia improved its

energy efficiency to the levels of comparable OECD countries, it could reduce its primary energy use by

almost one-third, an amount similar to the consumption of the United Kingdom. Potential savings of

natural gas alone,at 180 bcm,are close to Russia ?s net exports in 2010.

In the New Policies Scenario, cumulative CO2 emissions over the next 25 years amount to three-quarters

of the total from the past 110 years, leading to a long-term average temperature rise of

3.5°C. China's per-capita emissions match the OECD average in 2035. Were the new policies not

implemented, we are on an even more dangerous track, to an increase of 6°C.

“As each year passes without clear signals to drive investment in clean energy,the 'lock-in' of high-carbon

infrastructure is making it harder and more expensive to meet our energy security and climate

goals,” said Fatih Birol, IEA Chief Economist. The WEO presents a 450 Scenario, which traces an

energy path consistent with meeting the globally agreed goal of limiting the temperature rise to 2°C.

Four-fifths of the total energy-related CO2 emissions permitted to 2035 in the 450 Scenario are already

locked-in by existing capital stock, including power stations, buildings and factories. Without further

action by 2017, the energy-related infrastructure then in place would generate all the CO2 emissions

allowed in the 450 Scenario up to 2035. Delaying action is a false economy: for every $1 of investment

in cleaner technology that is avoided in the power sector before 2020, an additional $4.30 would need to

be spent after 2020 to compensate for the increased emissions.

__________________________________________________________

The World Energy Outlook is available for sale at the IEA bookshop. Journalists seeking a review copy

of the publication should send an email to ieapressoffice@iea.org.

About the IEA

The IEA is an autonomous organisation which works to ensure reliable, affordable and clean energy for

its 28 member countries and beyond. Founded in response to the 1973/4 oil cr isis,the IEA ’s initial role

was to help countries co-ordinate a collective response to major disruptions in oil supply through the

release of emergency oil stocks to the markets. While this continues to be a key aspect of its work, the

IEA has evolved and expanded. It is at the heart of global dialogue on energy, providing reliable and

unbiased research, statistics, analysis and recommendations.

International Energy Agency - 9 rue de la Fédération, 75739 Paris Cedex 15 - France

Tel: +33 (0)1 40 57 65 54 Fax: +33 (0)1 40 57 65 59 - www.iea.org

|

References

World Oil Capacity to Peak in 2010 Says Petrobras CEO

Oil depletion graphics

WEF Scenarios 2009 - A Reference Scenario

Das WEF Davos Open Forum und die FEK - eine Analyse

ecostory 5-2008 - The Davos Open Forum on Sustainability and Economic Growth

ecostory 3-2004 - Ein Forum für eine bessere Welt (A form for a better world)

|

|